ShengShu raised US$293 million on October 15, 2024, for artificial general intelligence (AGI) development amid surging AI data center energy storage demands. Reuters reports HongShan and Tencent led the Series A round.

Funding Accelerates AGI Compute Infrastructure

Source Code Capital and Gaorong Ventures joined the investment. ShengShu aims to build AGI models rivaling OpenAI’s o1-preview. Funds target hardware procurement, including GPUs, and talent hires.

China’s AI sector drew US$3.5 billion in 2024 investments, PitchBook data shows. ShengShu’s raise ranks among the top five. The firm plans exaflop-scale training in Shanghai data centers.

AGI Training Drives Massive Power Needs

University of California researchers estimate GPT-4 training consumed 1,800 MWh. Inference phases add terawatt-hours annually across deployments. AGI models demand 10x more compute, scaling power to gigawatt levels.

Global data centers consumed 460 TWh in 2023, per International Energy Agency (IEA). AI fueled 20% year-on-year growth. IEA projects 1,000 TWh by 2026, equaling 3% of global electricity.

Hyperscalers like Google and Microsoft deploy 100 MW facilities. Uninterrupted power supply (UPS) systems ensure zero-downtime training runs.

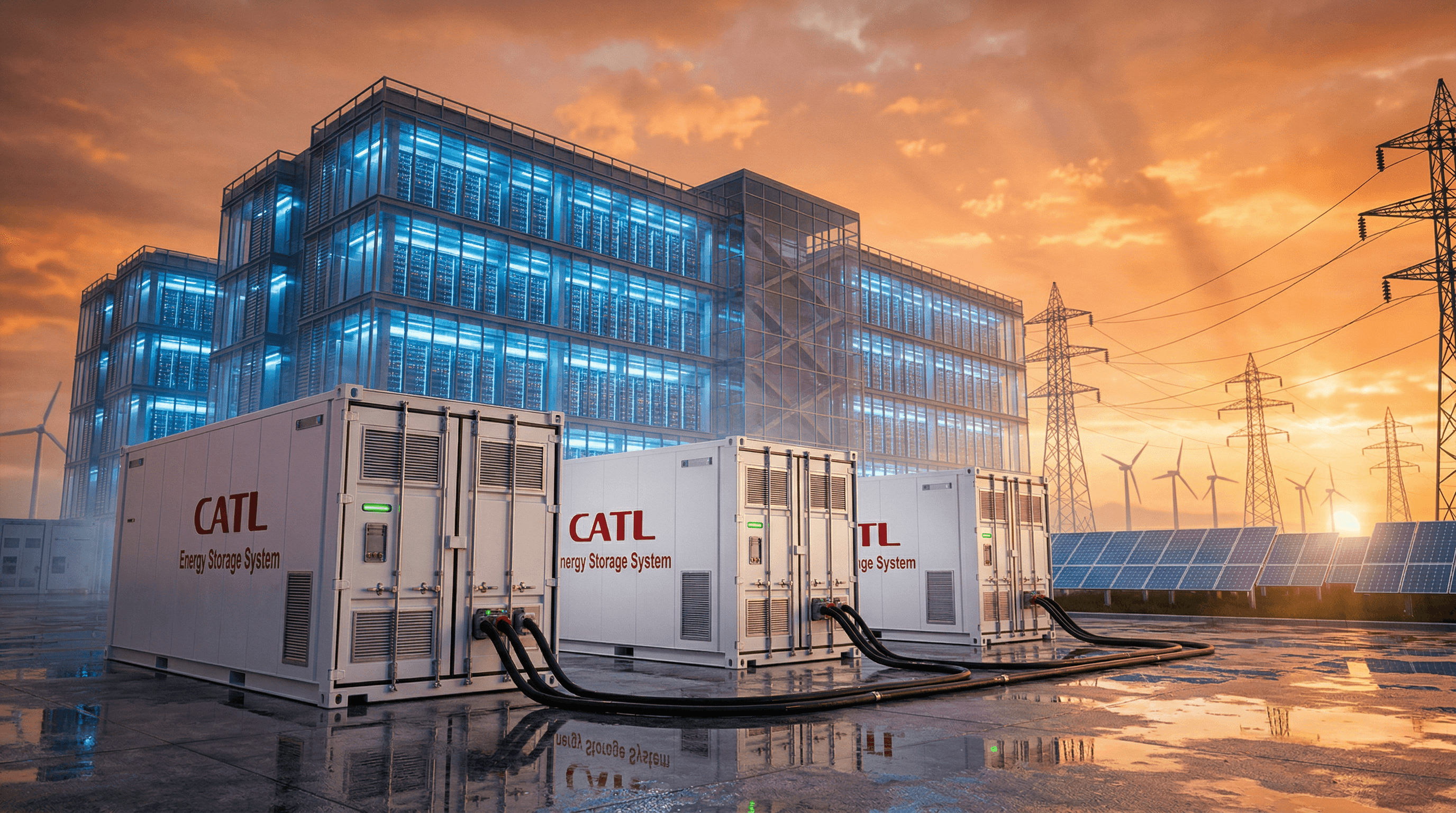

Lithium-Ion Batteries for AI Data Center Energy Storage

Lithium-ion batteries deliver 10-15 minutes of MW-scale bridge power during outages. A 50 MW data center requires 100 MWh packs for full backup.

Lithium-ion captured 40% of UPS market share by 2023, displacing lead-acid’s prior 80% dominance, Wood Mackenzie reports. Cells achieve 250 Wh/kg energy density at pack level.

System costs dropped to US$132/kWh in 2023, Benchmark Mineral Intelligence states. Data centers favor lithium iron phosphate (LFP) for thermal stability and 6,000 cycles at 80% depth of discharge (DoD), per IEC 62619 standards.

China Commands Global Battery Supply Chain

China manufactured 77% of global battery cells in 2023, totaling 1,200 GWh. CATL and BYD control 45% market share. Both supply Tesla Megapacks for grid storage.

CATL delivered 50 GWh of energy storage systems in H1 2024, earning RMB 70 billion (US$10 billion), company filings confirm. Eve Energy develops UPS modules with 200 Wh/L volumetric density.

China holds 90% of cathode production capacity despite graphite export restrictions. BloombergNEF predicts 50 GW of data center battery demand by 2030.

LFP chemistry sidesteps nickel volatility; prices rose 15% to US$18,000/tonne in 2024.

Renewables and Storage Enhance Efficiency

Batteries enable peak shaving and renewables integration. A 200 MW data center with 400 MWh storage cuts grid peak draw by 30%. LFP packs deliver 92% round-trip efficiency (RTE) at 0.5C discharge.

Google commissioned a 100 MW/400 MWh battery energy storage system (BESS) at its Finnish data center in 2024. Microsoft advances 1 GWh-scale projects globally.

Chinese LFP packs cost 20% less than US equivalents, per InfoLink Consulting. BYD tests vehicle-to-grid (V2G) with second-life EV batteries, retaining 70% capacity after 200,000 km and <10% annual degradation.

Commercial Challenges and Innovations

ShengShu targets 2025 data center launches, with AGI training ramping 2026-2028. Sites demand GWh-scale batteries at manufacturing readiness level (MRL) 9.

10 MWh UPS modules hit cost targets of US$100/kWh by 2027. CATL’s condensed battery packs reach 200 Wh/L density and 160 Wh/kg.

US Inflation Reduction Act (IRA) tariffs shield domestic production, but China exports 60% to APAC and Americas.

Competition Heats Up

Fluence Corporation reports a 1.5 GW BESS backlog. Sungrow shipped 80 GWh in 2023. Europe manufactures just 5% of global capacity.

ShengShu secures CATL priority supply contracts, fast-tracking AGI rollout.

Forward Outlook

ShengShu’s funding highlights AI data center energy storage as a bottleneck. GWh-scale deployments accelerate annually. China’s battery supremacy positions it to deliver 500 GWh for AI by 2030, per Rho Motion forecasts.